Why do central banks buy gold?

01 March 2022

Experimental monetary policy created market imbalances

Inflation concerns lead central banks to gold

A bar of gold always keeps its value. Crisis or not.

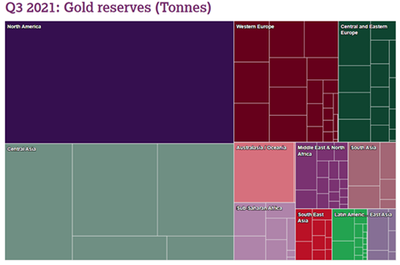

Central banks hold 36,000 tonnes of gold

Central banks are responsible for the value of their nation’s currencies and the value of these is subject to swings and market fluctuations.

Why do central banks buy gold?

Gold plays an important role in a country’s foreign reserves. As a result, central banks are significant holders of gold.

Gold is a unique commodity; with its duality as both a commodity and a monetary asset, it can act as a long store of value. The international gold market is deeply liquid, and it carries no counterparty risk, making it an ideal reserve asset for central banks to own.

Based on a study by the World Gold Council, the top four reasons central banks own gold are:

Long term store of value

Historical position

Performance during times of crisis

Effective portfolio diversifier

Notable heads of central banks have commented on the importance of increasing their gold position.

The De Nederlandsche Bank (DNB - Central bank of the Netherlands) said in 2021:

‘A bar of gold always keeps its value. Crisis or not. That gives a safe feeling. The gold holdings of a central bank are therefore a beacon of confidence.’

Similar sentiments were expressed by the National Bank of Poland, with Bank Governor Adam Glapinski stating the reasons for owning gold were clear:

‘Gold is characterised by a relatively low correlation with the main asset classes – especially the US dollar dominating the NBP reserve portfolio – which means that including gold in the reserves reduces the financial risk in the process of investing in them.’

Central banks hold 36,000 tonnes of gold

Central banks added 463 tonnes gold to their global reserves in 2021, an 82% increase on the 255 tonnes bought in 2020. Global central bank gold reserves are now just under 36,000 tonnes – the highest in 31 years.

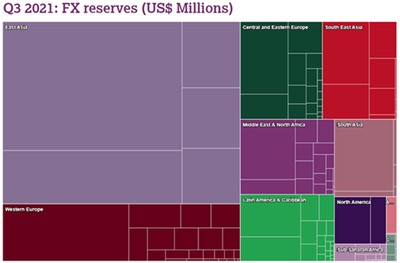

While the US has the largest dollar value and tonnage position in gold (left), East Asia has the largest portion of their FX reserves in gold (right).

Source: Central Banks; Federal Reserve Bank of St. Louis; International Monetary Fund; World Bank; World Gold Council

Last year, central bank buying of gold provided price support for this precious metal.

During the first nine months, there were several large purchases from central banks, such as Thailand and Brazil, in addition to surprise acquisitions from more developed economies like Ireland and Singapore, both adding to their reserves for the time in 12 years and 20 years respectively.

Up until 2009, central banks often sold gold to increase their holdings in US dollar denominated assets like US Treasury securities.

This trend began to reverse the following year, with central banks being net buyers of gold since 2010.

Central banks are expected to continue to add to their gold reserves in 2022 though it is unlikely to be as large as 2021.

Why inflation concerns drive central banks to gold

Central banks are responsible for the value of their nation’s currencies and the value of these is subject to swings and market fluctuations.

While central banks deploy various methods to manage monetary policy to smooth out economic cycles, the value of currencies change to reflect either the perceived strength or weakness of a local economy. For example, this can include increasing the money supply to avoid economic turmoil, though doing this risks the value of their local currency falling.

Experimental monetary policy in recent years has led to imbalances and market excesses, and many central banks are increasing their gold holdings as part of their foreign reserves to protect their position.

Inflation concerns leads central banks to gold

The Bank of Thailand (BOT) was the largest buyer of gold in 2021, adding 90 tonnes to their reserves. The Royal Bank of India (RBI) was the was the second largest, buying 77.50 tonnes bringing their total gold holdings to 754.1 tonnes – 6.22% of their total foreign reserves.

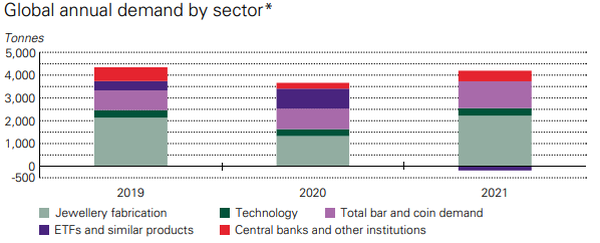

While central banks’ gold purchases only account for a small portion of total gold demand, central bank buying is expected to continue, not just for the above-mentioned central banks but for others around the world.

Source: Metals Focus; World Gold Council

Since 2010, central banks have been net buyers of gold as they move away from more traditional US dollar denominated assets like US securities.

Central banks are shifting further into gold leaving a declining presence of US dollars in their foreign reserves. This change in sentiment is attributed to both the stability of gold as a reserve asset, as well as concerns about long term falls in the US dollar.

Gold traditionally has an inverse relationship with the US dollar and helps mitigate the risk of inflation on central bank assets.

The value of currencies has varied significantly since the ending of the US dollar’s convertibility into gold. By purchasing more gold to add to their reserves, central banks are looking to hedge against a weakening US dollar and limit the impacts of inflation on their economies.

Until next time,

Shae Russell

Group Communications Manager